Is Your 'Diversified' Portfolio Actually Diversified? (Or are you taking a big bet on AI?)

Executive Summary aka TLDR: Markets are up across the board in 2026, and your portfolio is benefiting. U.S. stocks are more expensive than usual, but perhaps not at crisis levels. International markets are still looking attractive. AI is real and the companies driving it are exceptional, but a third of the S&P 500 is concentrated in just seven stocks, which is why we deliberately own those companies in a more balanced way. Your big takeaway: Tailored’s diversified model portfolios are positioned thoughtfully to perform through all different kinds of market environments.

Let's Start With the Good News…

Markets have had a strong first half of 2026. If you’ve glanced at your account statements recently, you’ve likely seen positive numbers across the board, and that’s worth acknowledging before we get into the nuances. Most investors with a diversified, balanced portfolio of about 70% stocks and 30% bonds are up 9% from January through June. Here’s how different parts of the market have performed so far this year:

A few things jump out here. First, smaller companies and international markets have actually outperformed the S&P 500 this year — which is a reversal from recent years when the S&P 500 dominated everything. Second, Fixed Income or bonds are barely positive at 0.1% YTD, which is a reminder that they serve a different purpose in a portfolio (stability and income) rather than growth.

A Quick Reminder on Diversification

The top performers of 2026 to date were actually bottom performers in recent years. No one asset class wins every year. That’s exactly why I spread your investments across different areas. Last year’s winner is rarely this year’s winner. Notice on the “quilt chart” how it is nearly impossible to pick any one year’s winner.

U.S. large-cap stocks (the S&P 500) have been the star of the last 15 years at 14.7% annually. But those returns don’t come in a straight line. The S&P 500 has had years like 2022 (-18.1%) and 2015 (+1.4%) mixed in with the great ones. Staying invested through those rough patches is what earns you the long-run average. The balanced portfolio of a mix of stocks, bonds, and other assets delivered 8.5% annually with considerably less stomach-churning along the way. For many of our clients, that smoother ride is worth the slightly lower average return.

But Don’t You Keep Saying that the US Stock Market is Expensive?

By historical standards U.S. stocks are on the pricier side. But “expensive” doesn’t always mean “about to crash.” The most common way to measure stock market valuation is the Price-to-Earnings (P/E) ratio. Think of it like a price tag: how much are investors paying today for every dollar of company earnings? A higher number means investors are paying more and expecting a lot of future growth.

At 20.0x, the market is above its historical average of 16.0x — but it is still below the peak during the dot-com bubble of 24.5x. So we’re in “elevated but not extreme” territory. What does this mean practically? It means the market has less room for error. If companies don’t deliver the earnings growth investors are expecting, stock prices could fall to adjust. It doesn’t mean run for the exits, it means be thoughtful about what you own.

International Stocks Still Offer Good Value Relative to the US

Here’s something that often surprises people: the U.S. market trades at a 20.0x P/E, but international developed markets (Europe, Japan, etc.) trade at just 15.5x and emerging markets are even cheaper at 11.2x. This is one reason I continue to include international exposure in client portfolios in a meaningful way. You get to participate in global growth at a lower price tag. For every $2 I invest in the US, I invest $1 outside the US.

The Magnificent 7: What They Are and Why They Matter to You

Maybe you’ve heard the term “Magnificent 7”. It refers to seven mega-cap technology companies that have dominated market returns in recent years: NVIDIA, Apple, Microsoft, Amazon, Alphabet (Google), Meta, and Tesla. Since 2020, these seven companies have returned 186% — more than double the Nasdaq’s 78% and nearly triple the S&P 500′s 73% over the same period. Since 2023 alone, they’re up over 335%!!!

The performance of the Mag 7 has been extraordinary. But it’s also created a concentration problem inside the S&P 500 that most investors don’t realize they have.

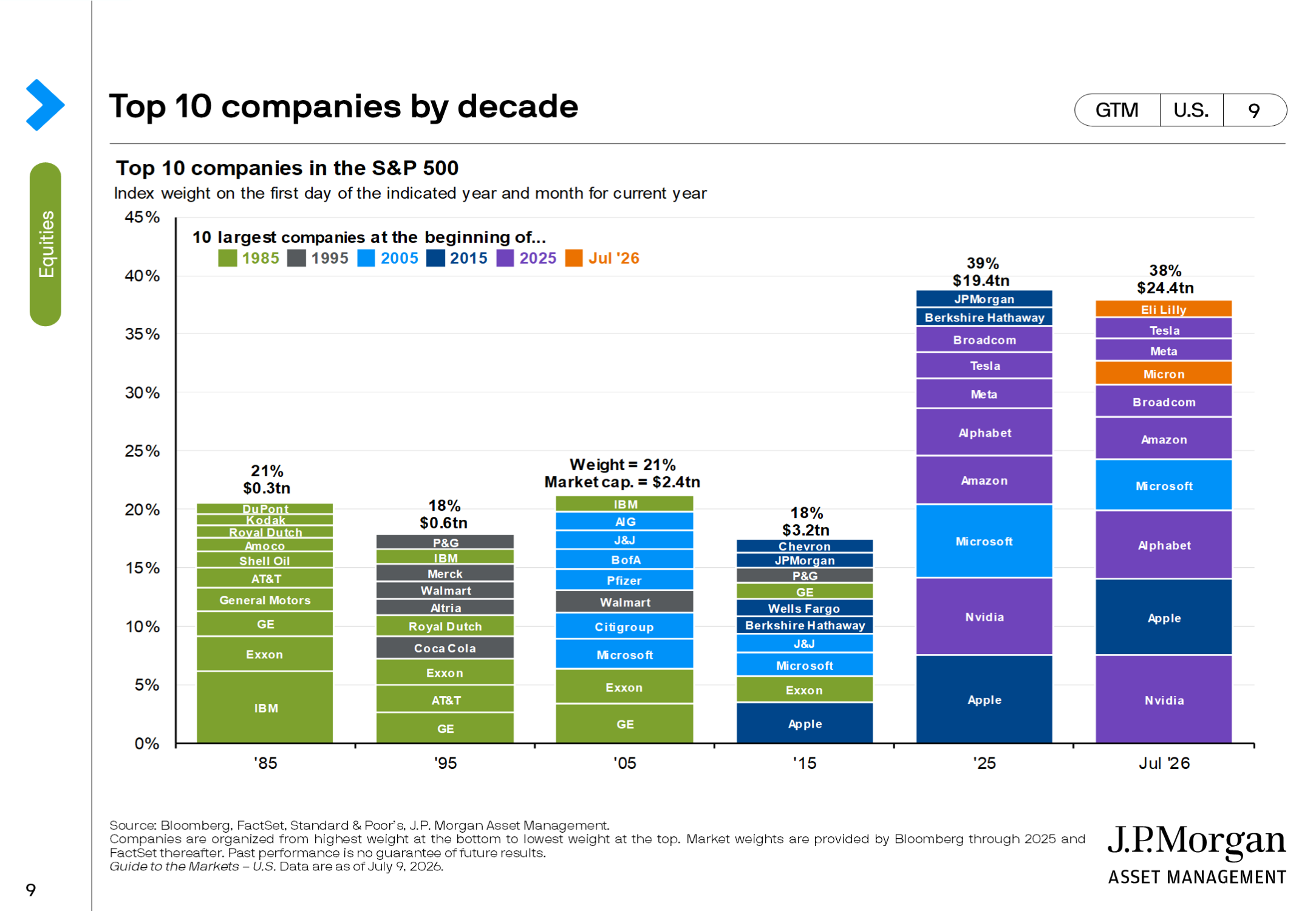

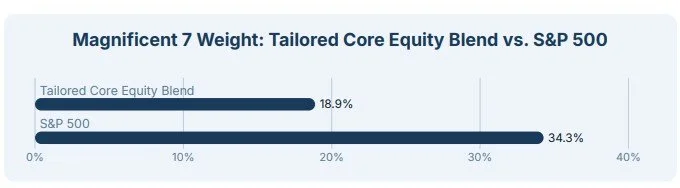

When you buy an S&P 500 index fund, you might think you’re buying 500 companies. In practice, the top 10 companies now make up 39% of the entire index and the Magnificent 7 alone accounts for 34%. That means nearly a third of your “diversified” index fund rises and falls with just seven stocks.

A bad quarter for NVIDIA or Apple has a much bigger impact on your portfolio than most people expect if you are only invested he S&P 500.

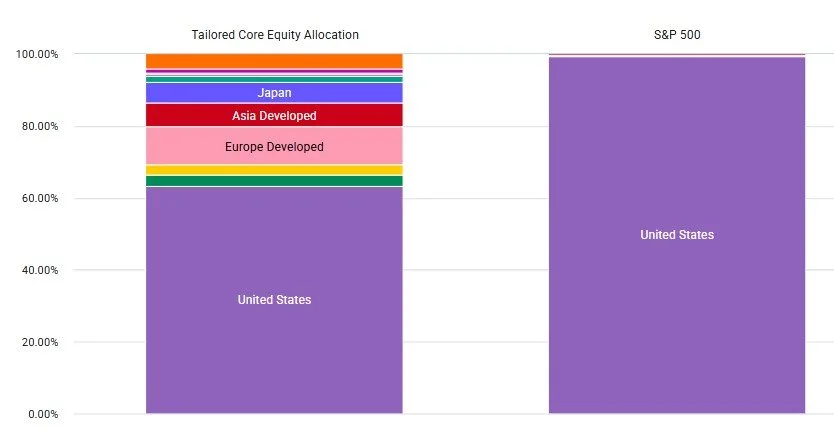

Our core equity models hold the Mag 7 companies but at roughly half the concentration of a pure S&P 500 portfolio. They are designed to keep meaningful exposure to these companies while not being entirely dependent on them. The international allocation does the heavy lifting here, spreading your dollars across hundreds of additional companies around the world, and the small & mid-cap US companies with less exposure to the technology sector also helps, (see regional chart below with Tailored on the left and the S&P 500 on the right.)

Everyone is talking about Artificial Intelligence

You can’t talk about markets in 2026 without talking about AI. The five largest technology companies — Google, Amazon, Meta, Microsoft, and Oracle — are collectively on track to spend over $758 billion on AI infrastructure this year alone. To put that in perspective, that’s more than the GDP of most countries.

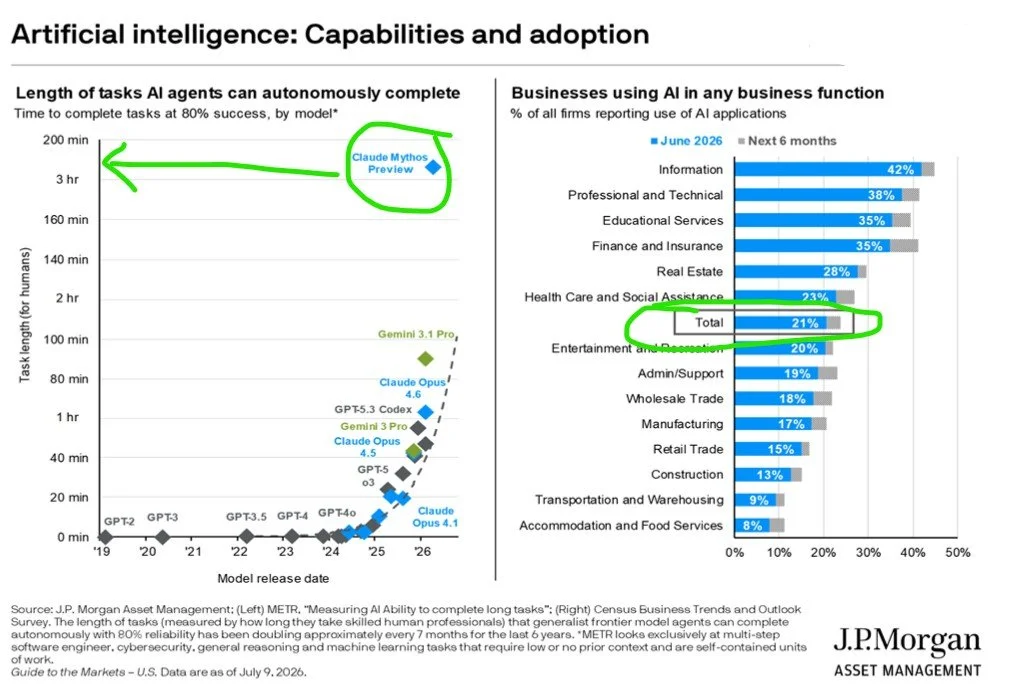

This spending is the reason NVIDIA’s stock over the last few years has been extraordinary — someone has to make the chips that power all of this. But it also raises an important question: is all this spending actually paying off? The short answer is: it’s getting there, but slowly. As of June 2026, only 21% of U.S. businesses are actively using AI. The finance and technology industries are leading the charge, but most of the economy — construction, food service, retail — is still in the early stages.

What’s remarkable is the productivity curve that new AI models are now hitting. The Claude Mythos Preview AI agent model is now able to complete a task that would have taken a human 3 hours in mere seconds or minutes. The labor market will see massive disruption with changes to how humans perform tasks in which industries and at what employment rate and corresponding wage.

AI is real and will make real changes to our economy and daily lives and the companies leading the charge have a huge opportunity ahead to eventually make profits off their investments. But today’s stock prices for AI-related companies (particularly NVIDIA) are pricing in years of continued dominance. If that plays out, great. If there are bumps in the road like a slower adoption curve, pushback from local governments to slow the pace of data center creation, or simply a quarter of missed earnings expectations, prices could reset quickly.

I estimate that roughly 7% of The Tailored Core Equity exposure is invested with “High-risk AI stocks” like NVIDIA, Broadcom and Micron. This compares to 13% of the S&P 500.

In short, we want to participate in AI’s growth but we don’t want your hard-earned life savings to significantly drop if the “AI bubble pops”.

In Closing…

The rest of 2026 calls for patience and discipline over chasing returns. The stock market has consistently performed well over the long-term through multiple new technological innovation cycles. The clients who stay the course through volatility and the headlines are the ones who capture those long-run returns. That’s what I’m here to help you do.

Questions? Let's Talk.

If anything here raised questions about your specific situation: your account, your allocations, or how you’re positioned for the rest of the year…please reach out. These are great conversations to have, and I’d love to connect.

Stacy Dervin, CFA, CFP® provides fee-only financial planning and investment management services in Eugene, Oregon. Tailored Financial Planning (TFP) serves clients as a fiduciary and never earns a commission of any kind. As a financial advisor, Stacy is on a mission to help Gen X and Gen Y be truly proactive about their financial futures.

This post is for informational purposes only and does not constitute tax or legal advice, research or an invitation to buy or sell any securities. Please consult a qualified tax professional regarding your specific situation and see our full disclaimer here.